Tax season is upon us, and at this time of year we at Skyline Wealth Management typically receive a number of tax-related questions. With that, taxation of Skyline’s REIT investments is a great topic to discuss.

The taxation rules described below are only applicable if the REIT investment is held as a non-registered account. They do not apply if the REIT investment is held in a registered account, such as an RRSP, RRIF or TFSA! Each type of registered account has its own tax procedures, which are not related to the type of investments inside the account. Stay tuned to these blog posts to find out more.

1. An ongoing monthly cash distribution (reflected by the current annual yield).

2. The potential for the value of your REIT Units (shares) to increase in market value over time.

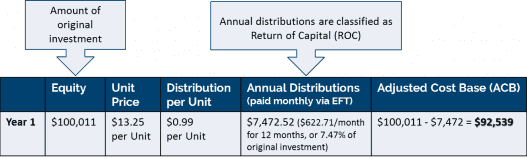

When you invest in a REIT, in some circumstances, your monthly cash distributions are not taxed as income. Rather, all or a portion are given to you in the form of Return of Capital (ROC).

These distributions result in a reduction of your Adjusted Cost Base (ACB).

Here is a hypothetical example to illustrate how the ACB is determined:

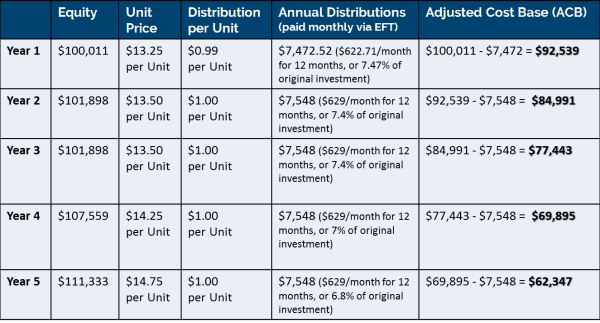

Now, let’s continue this example over a 5-year period.

In the right-hand column, you will see how the ACB is eroded over time. (If the investment is held long enough, the ACB may eventually go down to zero.)

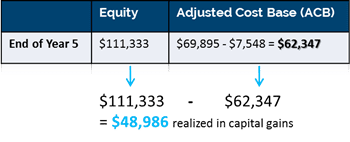

Your ACB determines how much you will realize in capital gains when you divest (redeem) your holdings. Based on our example, if an investor divested at the end of year 5, their capital gains would be calculated as follows:

Capital gains is the most tax-efficient treatment of investment returns. Capital gains are realized if/when you sell, or transfer ownership of, your investment (at a market value that is greater than what your original investment was). 50% of your realized profit (capital gains) is taxed at your individual tax rate.

So, for our example:

Again, this tax treatment is only applicable for Skyline REIT investments held in non-registered accounts. Stay tuned for Part 2, where we’ll briefly cover other types of taxation, and take a look at the taxation of investments held in registered accounts (RRSPs, RRIFs, TFSAs, etc.)

Best Regards,

Adam Batstone, CIM

Executive Vice President & Managing Partner,

Skyline Wealth Management

The contents of this article are for high-level, contextual purposes, and are not meant to replace advice from your accountant or any other tax advisor. We strongly suggest that an accountant or tax professional should be consulted prior to making an investment, and should be used on an ongoing basis once an investment is made. Skyline Wealth Management’s investments are available to qualified investors only. Contact us today to see if you qualify.